When markets are rising, risk feels invisible. When markets fall, it becomes the only thing that matters.

Over time, I’ve come to believe that successful investing is not primarily about chasing returns, it’s about managing risk intelligently and appropriately. Returns are a function of markets. Risk management is a function of discipline.

In this edition of Market Moves, I outline how I think about risk and the practical tools we use to manage it: asset allocation, diversification, currency hedging, uncorrelated assets, position sizing, and disciplined exit strategies like stop losses and trailing stops.

Risk Is Not Just Volatility

Many investors equate risk with short-term volatility. I don’t.

Volatility is uncomfortable, but permanent loss of capital is the real risk. Our objective is not to eliminate volatility — that’s impossible — but to structure portfolios so that temporary market movements do not turn into permanent impairment.

That philosophy shapes everything that follows.

1. Asset Allocation: The First Line of Defence

Asset allocation is one of the most powerful risk management tools available.

How much you allocate to equities/shares, both domestic and global, fixed income, cash, alternatives and other asset classes determines the majority of long-term outcomes. It matters more than stock picking and more than timing decisions.

Equities offer growth but can be volatile. Fixed income provides stability but lower long-term returns. Cash offers liquidity but erodes in real terms over time. Alternatives can provide diversification but must be selected carefully.

The key is alignment:

- Time horizon

- Income requirements

- Risk tolerance

- Liquidity needs

When allocation is aligned properly, market downturns become manageable rather than destabilising.

Importantly, asset allocation is dynamic. We adjust exposures as valuations, economic conditions and risks evolve.

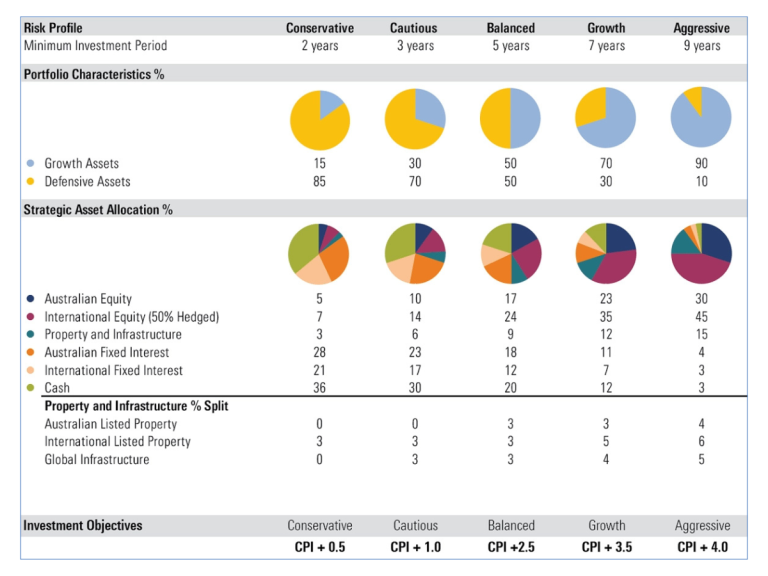

Morningstar’s defensive/growth asset class combinations:

2. Diversification: Not Just Owning “More”

True diversification is about owning assets that behave differently from one another.

Holding 20 Australian bank shares is not diversification. Holding global equities, defensive assets, and exposure across sectors and geographies is.

Diversification works because different assets respond differently to:

- Economic cycles

- Interest rate movements

- Inflation

- Geopolitical events

- Currency fluctuations

When one area struggles, another may provide stability.

However, correlations change over time. In crisis periods, many assets can fall together. That’s why diversification must be thoughtful, not mechanical.

3. Currency as a Risk Management Tool

For Australian investors, currency exposure is a critical – and often overlooked – risk lever. The Australian dollar (AUD) has risen significantly in early 2026, reaching a three-year high against the US dollar (USD) and a five-year high on its trade-weighted index. As at 19 February 2026, the AUD is trading around US$0.704, up from an average of approximately US$0.645 in 2025.

Currency moves of this magnitude can materially influence portfolio outcomes.

The AUD is closely tied to global growth and commodity cycles. During global risk-off events, it often weakens. For investors holding offshore assets, this can provide a natural hedge: foreign investments may decline in local terms but appreciate when translated back into Australian dollars.

When the AUD is elevated relative to recent history, we think carefully about the risk/reward trade-off of hedging versus maintaining unhedged global exposure.

- Hedged exposure reduces volatility arising from currency movements.

- Unhedged exposure can provide downside protection if the AUD weakens during periods of global stress.

There is no universal rule. Currency positioning is considered within the broader portfolio construction process, balancing valuation, macroeconomic conditions and overall risk objectives.

4. Uncorrelated Assets: Building Shock Absorbers

Adding uncorrelated or low-correlation assets can materially reduce overall portfolio volatility.

Examples might include:

- Gold in periods of uncertainty

- Certain alternative strategies

- Absolute return funds

- Select infrastructure or real assets

The objective isn’t to chase exotic investments. It’s to create structural shock absorbers within the portfolio.

When equity markets fall sharply, uncorrelated assets can cushion the drawdown, allowing investors to stay disciplined rather than react emotionally.

5. Position Sizing: Risk is Not Equal Across Ideas

Not every investment deserves the same allocation.

High-conviction, high-quality holdings may justify larger positions. More thematic, cyclical or higher-volatility exposures should typically be sized more modestly.

Position sizing forces us to ask a simple but important question:

“If this investment is wrong, how much damage can it do?”

Even strong ideas can underperform. By controlling position size, we ensure no single investment can materially impair the overall portfolio.

This is where a core and satellite framework becomes particularly valuable.

The core of the portfolio is allocated to high-quality, diversified exposures designed to deliver steady, long-term compounding. These positions tend to be larger, more stable, and aligned with strategic asset allocation.

The satellite positions are smaller, more tactical allocations. These may include thematic opportunities, shorter-term trades, or areas with higher potential upside — but also higher risk.

By structuring portfolios this way, we allow for measured opportunism without compromising overall stability. The core provides resilience; the satellites provide flexibility and return enhancement.

This disciplined approach to sizing ensures that enthusiasm never overrides risk control.

6. Stop Losses and Trailing Stops: Enforcing Discipline

Markets are emotional. Rules protect us from ourselves.

A stop loss sets a predefined level at which a position is reduced or exited if it falls below a certain price. It is designed to limit downside.

A trailing stop loss moves upward as the asset price rises, locking in gains while allowing upside participation.

These tools are particularly useful for:

- Tactical positions

- Higher-volatility assets

- Thematic exposures

- Shorter-term trades

They are less appropriate for long-term core holdings, where short-term volatility is expected.

Used properly, stop mechanisms remove emotion from the decision process and preserve capital for better opportunities.

7. Liquidity: Flexibility When it Matters Most

Liquidity is an often underappreciated element of risk management.

We ensure portfolios maintain an allocation to assets that can be accessed or sold quickly without materially impacting price — typically cash or highly liquid securities.

It’s also important to recognise that not all managed investments offer the same liquidity. Redemption periods vary depending on the underlying assets.

- Listed securities and many liquid funds typically settle within T+2 or T+3 days.

- Some alternative or private market strategies may require 30–90 days’ notice.

- Unlisted property or real asset funds may have redemption periods measured in months, and in stressed conditions, withdrawals can be restricted.

The more illiquid the underlying asset – such as property or private markets – the longer the capital may be tied up.

This doesn’t make these assets inappropriate, but it does mean liquidity must be managed at the portfolio level.

Maintaining sufficient liquidity provides two key advantages:

Defensive flexibility

The ability to meet income needs or rebalance without selling long-term assets at depressed prices.

Opportunistic flexibility

The ability to deploy capital into high-quality assets when volatility creates attractive entry points.

Cash may appear unproductive in strong markets, but in volatile environments, liquidity provides resilience and the capacity to act when it matters most.

8. Accepting That Risk Cannot Be Eliminated

No strategy eliminates risk entirely.

There will always be:

- Economic shocks

- Policy and regulatory changes

- Geopolitical events

- Market overreactions

Markets are not driven by fundamentals alone. They are also influenced by sentiment — the collective mood of investors.

Market sentiment reflects how optimistic or pessimistic participants feel at a given point in time. When sentiment is strong, investors may overlook risks and push valuations higher. When sentiment deteriorates, fear can drive prices below intrinsic value, sometimes indiscriminately.

Importantly, sentiment can change faster than fundamentals.

This is why markets often overshoot in both directions — rising further than justified during periods of optimism, and falling more sharply than fundamentals alone would suggest during periods of stress.

Risk management acknowledges this reality. We cannot predict precisely when sentiment will shift, but we can structure portfolios so they are resilient when it does.

The goal is not perfection. It is preparation.

Well-constructed portfolios should be able to absorb shocks, navigate swings in sentiment, and continue compounding over time.

That requires discipline, structure and patience.

9. Risk Management Is About Staying Invested

Perhaps the most important function of risk management is psychological.

Investors who take too much risk often sell at the worst possible time. Investors who structure portfolios thoughtfully are far more likely to remain invested through volatility.

Compounding only works if you stay in the game.

By combining:

- Thoughtful asset allocation

- Genuine diversification

- Currency awareness

- Exposure to uncorrelated assets

- Sensible position sizing

- Clear exit rules

- Adequate liquidity

we aim to reduce the likelihood of permanent capital loss while preserving long-term growth potential.

Final thoughts

Markets will always cycle between optimism and fear. Headlines will oscillate between euphoria and crisis.

Risk management is not about predicting every outcome. It is about preparing for uncertainty.

In my view, managing risk is less about bold moves and more about consistent discipline. The steady application of sound portfolio construction principles is what allows investors to navigate volatility and continue compounding wealth over the long term.

As always, successful investing is not about avoiding risk, it’s about understanding it, pricing it appropriately, and structuring portfolios so that risk becomes manageable rather than destructive.

That is how we think about it.

| RISK | WHAT TO WATCH | |

|---|---|---|

|

Geopolitics |

Ukraine, Middle East, Taiwan tensions |

Trade Wars |

RISK

WHAT TO WATCH

Geopolitics

| RISKS | WHAT TO WATCH |

|---|---|

| Geopolitics | Ukraine, Middle East, Taiwan tensions |

| Trade Wars | US-China tariffs, Mexico sanctions |

| Sticky Inflation | Especially in energy and services |

| Growth Concerns | Weakening consumer demand |

| US Debt | $1.9T deficit + $1T in interest payments |

| Climate Risk | Infrastructure damage and supply chain disruption |

| Valuation Risk | Over concentration in megacap tech |

Tony Raikes

CPA. B.Acc Dip.FP Grad.Cert.Mgt

Private Client Advisor

Authorised Representative No. 00448193

Prince Wealth Founder and Financial Adviser Tony Raikes utilises a variety of advanced risk management strategies to protect clients’ portfolios and is dedicated to providing a comprehensive financial planning experience, empowering clients to make confident and informed decisions about their financial future.