After an exceptional run for many asset classes in 2025, one theme continues to stand out as we move into 2026: commodities. Precious metals, base metals and critical minerals have all delivered strong performance, supported by a mix of cyclical tailwinds and longer-term structural forces.

Commodity markets are inherently cyclical. Strong demand and tight supply tend to push prices higher, but those higher prices eventually encourage new supply, causing prices to settle back toward more normal levels. However, the current cycle appears unusual in that supply constraints, geopolitics and strategic stockpiling are reinforcing price strength across multiple commodities at the same time.

This creates both opportunity and risk — making disciplined exposure and position sizing critical.

Precious Metals: Gold and Silver Back in the Spotlight

Gold and silver were standout performers in 2025. Gold recorded dozens of all-time highs, supported by:

- Persistent central-bank buying

- Strong ETF inflows

- Elevated geopolitical risk

- Concerns around fiscal sustainability and government debt

ETF holdings in gold more than doubled during 2025, reaching record levels, reinforcing gold’s role as a store of value and portfolio insurance rather than simply a tactical trade.

Silver’s move was even more dramatic. While it shares gold’s monetary characteristics, silver also benefits from industrial demand, particularly from solar, electronics and electrification. This dual role often makes silver more volatile — rising faster in bull phases and falling harder in downturns.

Gold vs Silver – 2025 in Review, 2026 Outlook

- Gold (2025): +70% (approx.)

- Silver (2025): +170% (approx.)

Looking ahead to 2026, major banks expect continued support:

- Gold forecasts cluster around US$4,800–$5,000/oz

- Silver remains sensitive to sentiment but faces tight inventories

An important nuance for investors: large-cap gold miners tend to track the gold price closely, while smaller miners offer higher leverage – for better or worse – to rising prices and operational outcomes.

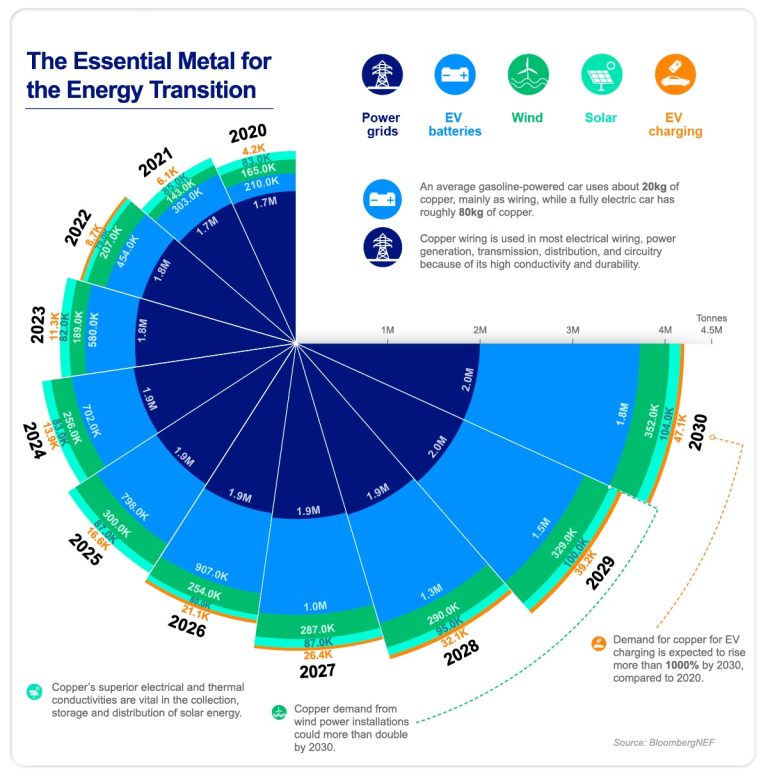

Copper: Structural Shortages Meet the Energy Transition

Copper is increasingly viewed as a strategic metal, central to electrification, EVs, renewable energy and AI infrastructure.

While demand has been resilient, the real story is on the supply side:

- Declining ore grades at major global mines

- Ageing assets in Chile and Peru

- Project delays, cost blowouts and labour shortages

- Years of underinvestment in new discoveries

Multiple analysts expect 2026 to mark one of the most severe copper deficits in over two decades, with deficits potentially exceeding 500,000 tonnes .

Even after strong price gains in 2025, forecasts for 2026 cluster in the US$11,000–$13,000/t range, with some bullish scenarios pushing higher if supply disruptions persist.

Copper remains cyclical, but the electrification theme may dampen — not eliminate — the traditional boom-bust pattern.

Rare Earths: Strategic Minerals and Geopolitics

Rare earth elements sit at the intersection of technology, defence and geopolitics. Supply chains are highly concentrated, with China dominating both mining and processing.

Greenland has re-emerged as a focal point in global discussions around rare earth security, highlighting Western efforts to diversify supply and reduce strategic dependence.

While demand from EVs, wind turbines and electronics is compelling, rare earths carry heightened geopolitical, regulatory and ESG risk, making stock selection especially important.

How We’ve Positioned Client Portfolios

Direct Equity Exposure

ETFs and Listed Vehicles

Gold:

- (ASX:NUGG): VanEck Gold Bullion ETF (physical gold bullion exposure, Australian-sourced gold).

- (ASX:GOLD): ETFS Physical Gold (commonly used ASX code for a physical gold bullion ETF).

Silver:

- (ASX:ETPMAG): ETFS Physical Silver (silver bullion exposure via exchange-traded product)

Copper:

- (ASX:WIRE): Global X Copper Miners ETF (equity-based copper miners exposure rather than direct copper).

ETFs can provide diversified exposure with lower company-specific risk, though they remain fully exposed to commodity price cycles.

Understanding the Risks: Commodity Investing is Not Set-and-Forget

Mining equities sit at the higher-risk end of the equity spectrum. They are effectively leveraged bets on both the underlying commodity price and the company’s execution.

Key risks include:

- Commodity price risk: Price moves are often amplified in share prices

- Operational and cost risk: Labour, energy and input cost inflation

- Geological and project risk: Reserves and grades can disappoint

- Jurisdiction and ESG risk: Policy changes can materially alter economics

- Financing and dilution risk: Particularly for juniors and developers

- Volatility and liquidity risk: Especially in small-cap and rare earth names

Importantly, gold miners are not the same as holding physical gold. They retain equity-like volatility and can underperform bullion if costs rise or management under-delivers.

| RISK | WHAT TO WATCH | |

|---|---|---|

|

Geopolitics |

Ukraine, Middle East, Taiwan tensions |

Trade Wars |

The Bottom Line

Commodities are cyclical — but the current cycle is being shaped by structural supply constraints, geopolitical realignment and the energy transition.

Gold and silver continue to play a role as portfolio diversifiers and hedges. Copper and rare earths offer exposure to long-term industrial demand, but with higher volatility and execution risk.

For 2026, we see commodities as an important allocation, not a one-way bet. Position sizing, diversification and quality bias remain central to how we manage this exposure for clients.

As always, we continue to reassess the cycle — because in commodities, timing matters almost as much as conviction.

RISK

WHAT TO WATCH

Geopolitics

| RISKS | WHAT TO WATCH |

|---|---|

| Geopolitics | Ukraine, Middle East, Taiwan tensions |

| Trade Wars | US-China tariffs, Mexico sanctions |

| Sticky Inflation | Especially in energy and services |

| Growth Concerns | Weakening consumer demand |

| US Debt | $1.9T deficit + $1T in interest payments |

| Climate Risk | Infrastructure damage and supply chain disruption |

| Valuation Risk | Over concentration in megacap tech |

Tony Raikes

CPA. B.Acc Dip.FP Grad.Cert.Mgt

Private Client Advisor

Authorised Representative No. 00448193

Prince Wealth Founder and Financial Adviser Tony Raikes utilises a variety of advanced risk management strategies to protect clients’ portfolios and is dedicated to providing a comprehensive financial planning experience, empowering clients to make confident and informed decisions about their financial future.